I came across ENSV this week and it checked enough boxes to pique my interest.

ENSV is an oilfield services company providing frac water heating, hot oiling and acidizing, and water transfer services across many of the major domestic oil and gas basins in the U.S (DJ/Niobrara, Bakken, Marcellus and Utica Shale, the Jonah Field, Green River and Powder River Basins, the Eagle Ford Shale, and the Stack and Scoop). The business is inherently cyclical with many of the services needed in colder weather periods, making the 1st and 4th Quarter about 70% of annual activity.

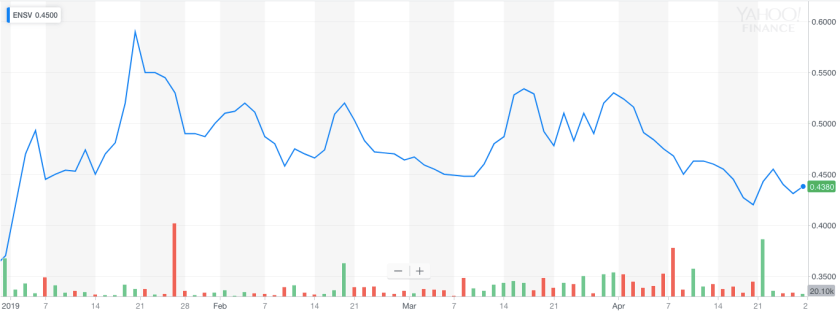

Like anything oil related, it fell throughout 4Q 2018.

However, as the title suggests, the company hasn’t recovered at all YTD.

However, as the title suggests, the company hasn’t recovered at all YTD.

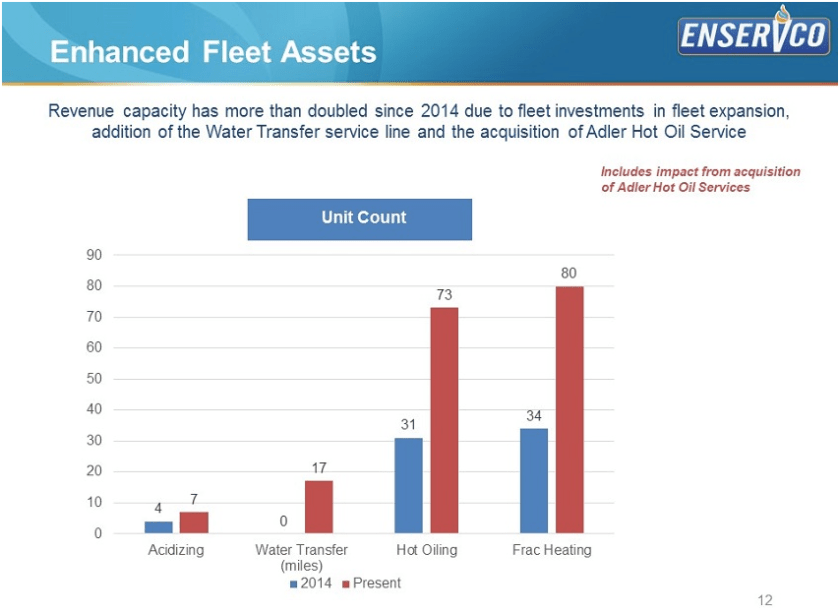

The company survived the depths of the last cycle without too many bruises, and came out on the other side with a much improved fleet in terms of size and service offerings like Water Transfer (revenue grew ~100% to $4.2mm in ’18) to differentiate vs. customers.

2018 results were good. Revenue grew 26.5% to $46.9mm while EBITDA grew 29% to $4.9mm. (For comparison’s sake, ENSV’s peaks reached during the last cycle occurred in 2014 with Revenue of $56.6mm and EBITDA of $11.5mm.)

Results look even better than ‘good’ given the cyclicality: the 4Q18 meltdown in oil prices paused many oil companies’ spending until 2019 and As a result 4Q Revenue only grew 13% while EBITDA fell 11%.

The company pre-reported some 1Q 2019 numbers on 4/25/19: Revenue of $26.2mm, +29% YoY, with EBITDA and Net Income expected to grow YoY also.

The company’s balance sheet is one aspect that does give me some pause, at first glance, with Total Debt of $38mm. However, when you account for the fact that the CEO, CFO, and COO all have long-term options as part of their incentive comp that only vest if/when Debt/EBITDA reaches 1.5x, I expect debt reduction to be a focus throughout 2019 and beyond.

The largest shareholder is a small and micro cap hedge fund, Cross River Partners, that owns 23% of the company and has a seat on the board.

Conclusion

ENSV checks a lot of boxes of being an interesting opportunity. Management has the proper incentives in place: skin in the game and LT options vesting on Debt/EBITDA 1.5x/share price reaching $2.25. While the business is competitive, ENSV’s scale in this niche will be able to beat smaller regional operators. I also wouldn’t be surprised to see more tuck-in acquisitions throughout 2019. The price is where I pause for now, in a world where oil remains > $50/bbl consistently I think ENSV’s EBITDA could get back to the peaks seen in 2014 and surpass it. With a current EV ~$60mm, at $11mm EBITDA, EV/EBITDA is already in the range of its peers, 5-7x EV/EBITDA.

I would need to see some more information around the utilization trends of the company’s rigs. While I recognize the increase in fleet size, at what point do we see that paying off? Revenue is getting close to 2014 peaks but EBITDA isn’t despite this increase. I’ll also be interested in commentary around the Alder acquisition on the Q1 19 call. ENSV issued an 8-K in April that disclosed the purchase price was dropping by $2mm. Has the performance lagged? Were there items not disclosed prior to purchase? I’ll be staying on the sidelines for now, but this is one I will be watching closely going forward.