Why should you care about Cyan? They continue to prove their market leading digital security offering by booking new contracts, the most noteworthy a global group agreement with Orange. This adds a higher level of certainty to financial results over the next 2-3 years (pending successful rollout). Despite this, the company is trading at ~6.0-7.0x EBITDA vs. peers in the low to high teens. The stock has suffered from a 2019 EBITDA cut (increased investment spend but increased 2021 EBITDA guidance as a result) and the fact it trades on a lower German exchange (plan to uplist to Frankfurt in 2020). It was announced on 11/13/19 that the company has retained Lazard for a strategic review, “To fully capitalize on such growth opportunities, the management board of cyan AG has decided to evaluate potential options regarding its US Expansion Strategy.”

Cyan is a digital security company that offers white-label solutions to mostly mobile network operators, but also other financial companies and governments. The slide below from their Investor Presentation best summarizes what offerings they bring to the market.

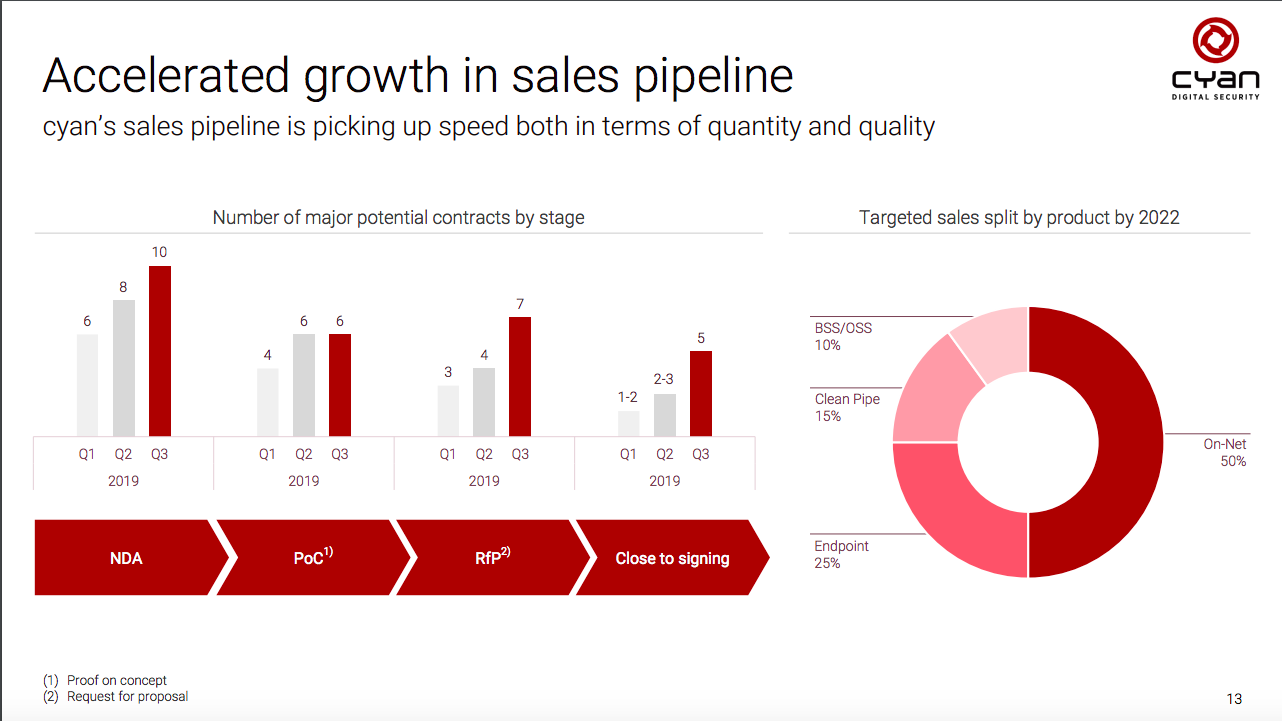

I’m not an expert on the technology by any means. Cyan will tell you their key differentiation vs. peers is the ability to offer both On-Net and Endpoint services at scale. Looking at the contract wins over the past year+, I tend to believe them.

The company has successfully implemented their programs for T Mobile in Austria* and Poland and have announced the following:

- 11/2018 Aon strategic partnership on digital security

- 12/2018 Orange global group 6 year contract

- 7/2019 T-Mobile Austria contract extended, ahead of schedule, by 1.5 years until mid 2022. Added integration of fixed network customers into the customer spectrum

- 7/2019 Telecom Argentina proof of concept installation

- 7/2019 Wirecard strategic partnership

- 11/2019 Flash Mobile sale of 60mm new licenses across LatAm

The Orange contract is the biggie. Across the entire system Cyan will be in 28 countries, exposed to 260mm fixed and residential customers, across residential and business accounts. Implementation has been ongoing throughout 2019 with rollout in France in Q4 2019 with the rest of Europe and Africa to follow in Q1 2020.

Based on the estimated implementation rate of this contract, Cyan issued 2021 guidance of Revenue of at least €60mm. This has since increased to Revenue of at least €75mm and an EBITDA margin target of 50% after the company increased investment spending to capture the additional new business opportunities available. They included the following slide in their Q319 results.

I think the 2021 guidance is conservative. The biggest driver right now will be the successful implementation of the Orange contract. Cyan assumptions here are a 6.4% adoption rate with an average ARPU of €1.56/year. This will vary between €1 to €4 depending on the different areas as Europe will be a lot different than Africa. The T-Mobile Austria and Poland adoption reached 25% in the first 3 years, here the ARPU was between €1.50 to €2. Based on the varying geographies in the Orange deal there will likely be different sales strategies such as opt-in, opt-out, and mandatory plans. As Orange shares in the revenue, they have an incentive to lean towards stickier strategies such as opt-out and mandatory plans that would vastly increase the 6.4% adoption estimate.

Even if we don’t assume any upside to adoption, Cyan currently is trading at <6.5x 2021 EBITDA. Give a low-end peer group multiple of 12x EBITDA, shares would trade at nearly €40 vs. ~€20/share today. That doesn’t include any additional contract wins or the value this asset could have to a strategic with the ability to penetrate the U.S. market. The strategic review outcome is a win-win in my mind: either/or the company lists in the U.S. bringing much deserved attention to the name, or the company sells itself at what I think would be a value at least 2x current prices.

*Worth noting Cyan did a 10% capital raise in July to support the increased level of growth spending and it was done at €28/share. The major shareholders all participated and even agreed to a 12-month lock-up. Management holds ~8% of shares outstanding and ~38% is split between 3 Austrian entrepreneurs.