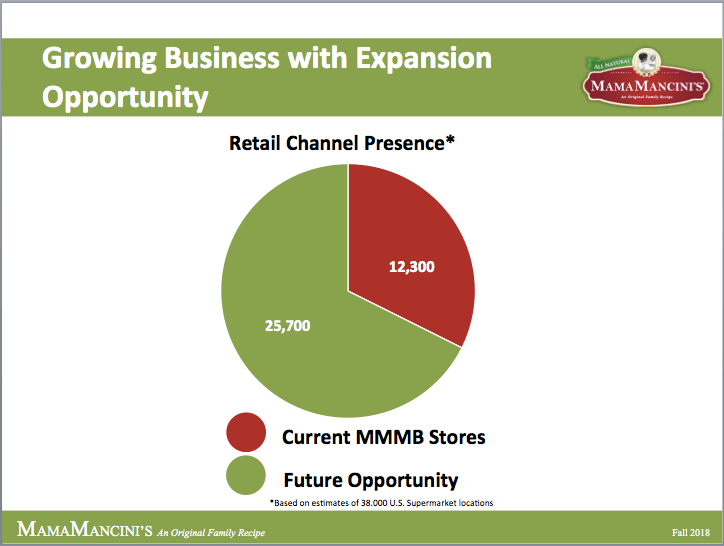

I’m going to sound like every value investing blog or quarterly letter when I say the more boring an idea, the better. MamaMancini’s (MMMB) fits this perfectly. Selling branded meatballs and other Italian dishes, MMMB is taking advantage of a trio of trends in consumer packaged foods that are actually driving growth: 1) Natural and Organic 2) Freshly prepared foods 3) Frozen foods. The company successfully grew the top-line at 43% in Fiscal 2017 and 53% in Fiscal 2018, leading to a profitable and FCF positive 2018. This growth came as MMMB was able to increase their product placement to 43,300 SKUs in 12,500 locations as of 7/31/18 from 32,000 SKUs at 10,100 locations as of 1/31/16.

The stock has been a laggard over the last year, exacerbated by a weak Fiscal 2Q 2019 (7/31/18) as changes in multiple purchasing offices of MMMB’s customers caused sales to drop vs. 2Q18. Despite this, the stock is offering investors a great deal as growth is likely to continue in the coming quarters as MMMB management has laid a solid base for the company with catalysts upcoming for significant stock price appreciation.

Catalysts:

- $40mm annual run rate of sales by end of fiscal year: management expects SKUs to increase by 7-10k placements to 50-53k total. A $40mm annual run rate would mean a resumption of ~25% growth by Fiscal 4Q19 (1/31/19)

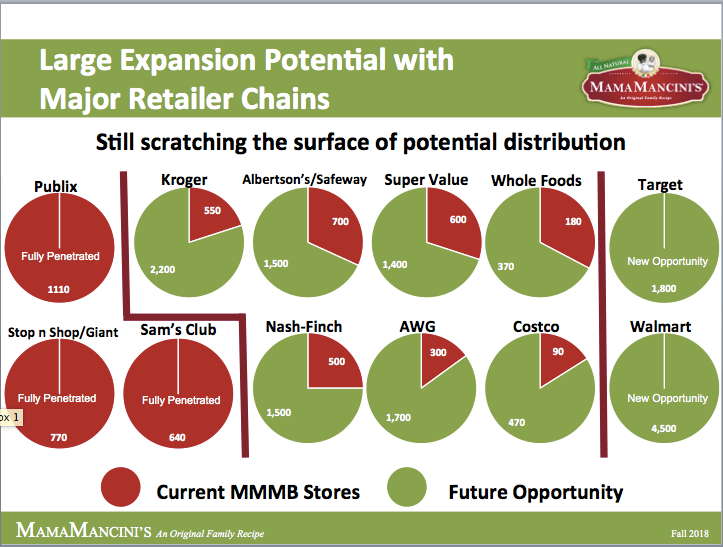

- Continued growth in Fiscal 2020: MMMB indicated a major national retailer has strongly indicated a start date for selling our products next spring. As you can see below the company still has only entered about 32% of available locations.

- Strategic Alternatives Initiative: MMMB retained Akin Bay Company in partnership with Kernick Advisory Group to investigate strategic options for MMMB shareholders “Given the current strong U.S. economic environment, management and the Company’s Board of Directors believe that this is an appropriate time to evaluate the Company’s market position and prospects and investigate if there are alternatives where shareholder value can be substantially enhanced. Potential options could include, but not be limited to, strategic acquisitions, a merger with, or purchase by a larger strategic food company or investors or recapitalization of the Company. There is no guarantee that any transaction will occur. However, given the positive fundamentals of the economy and MamaMancini’s, we believe that our shareholders deserve a comprehensive review of our options. We intend to further comment on this process when appropriate.” Current CEO and the largest shareholder (21%) of MMMB, Carl Wolf, has extensive experience building and selling consumer branded products, from the most recent 10-K, “ Wolf was the founder, majority shareholder, Chairman of the Board, and CEO of Alpine Lace Brands, Inc., a NASDAQ-listed public company with over $125 million in wholesale sales. He also founded, managed, and sold MCT Dairies, Inc., a $60 million international dairy component resource company. Other experience in the food industry includes his role as Co-chairman of Saratoga Beverage Company, a publicly traded (formerly NASDAQ: TOGA) bottled water and fresh juice company prior to its successful sale to a private equity firm.”

- If nothing comes of the strategic review uplisting to Nasdaq will increase liquidity and visibility for the company and stock

Valuation:

MMMB recently completed a plant expansion, following the acquisition of its supplier Joseph Epstein Foods, that will allow for $50-60mm of annual sales at current production plans. A great benefit of this company is the operational leverage, which has been evident throughout the growth period beginning in Fiscal 2016.

At a $60mm sales level, 40% gross margin, 0.5% of sales to R&D, and SG&A of $12mm, the company produces EBIT of $11.7mm. Compare that to the fully diluted market cap, as of 11/26/18, of $32.3mm. This is a longer-term target so let’s look at something that could be achieved in Fiscal 2020. Let’s assume a $40mm annual sales target, which is conservative given that this run rate is expected to be achieved by 4Q19. Assuming this level of sales with 40% gross margin, 0.5% of sales to R&D, and SG&A of $10mm, the company produces EBIT of $5.8mm. Currently you’re paying 5.5 times operating income for a high growth company, with a runway for continued growth, and a number of catalysts that could uncover value for shareholders.

Along with the CEO Wolf, insiders own close to 50% of outstanding shares. This is a unique, and almost boring, opportunity where investors can invest alongside a leader in the industry who has a demonstrated track record of success. If the company continues to execute on its growth plan I think the stock could double from current levels. A sale of the company would likely limit this upside potential, but would make sense given the investment necessary to surpass the current $50-60mm sales capacity the company currently has.

Full disclosure, I currently own shares of MMMB. This is simply an opinion and not a recommendation to buy.

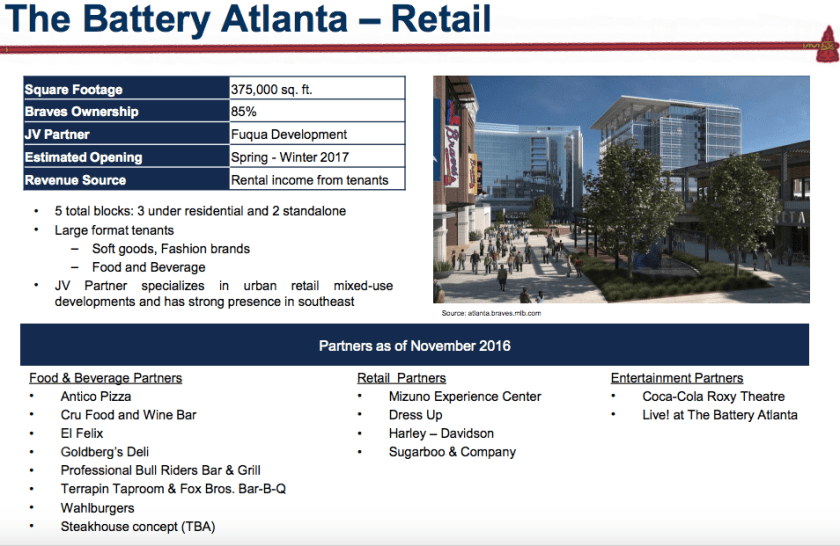

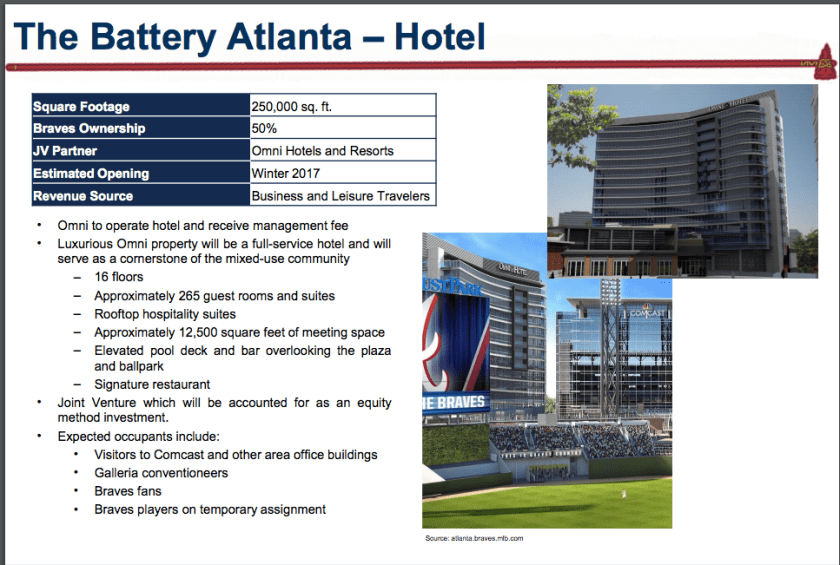

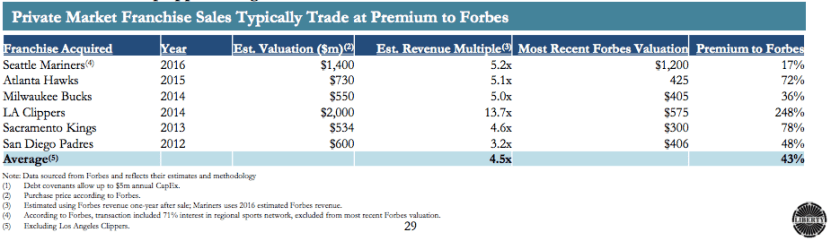

(Source: Liberty Media investor presentation)

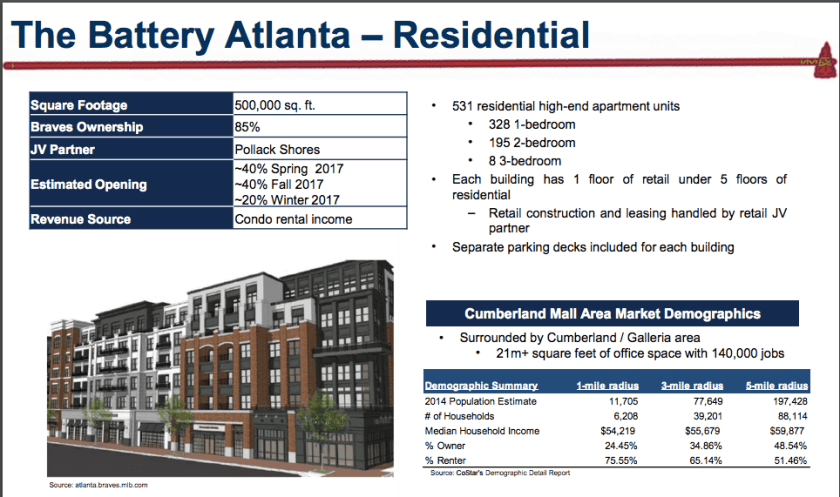

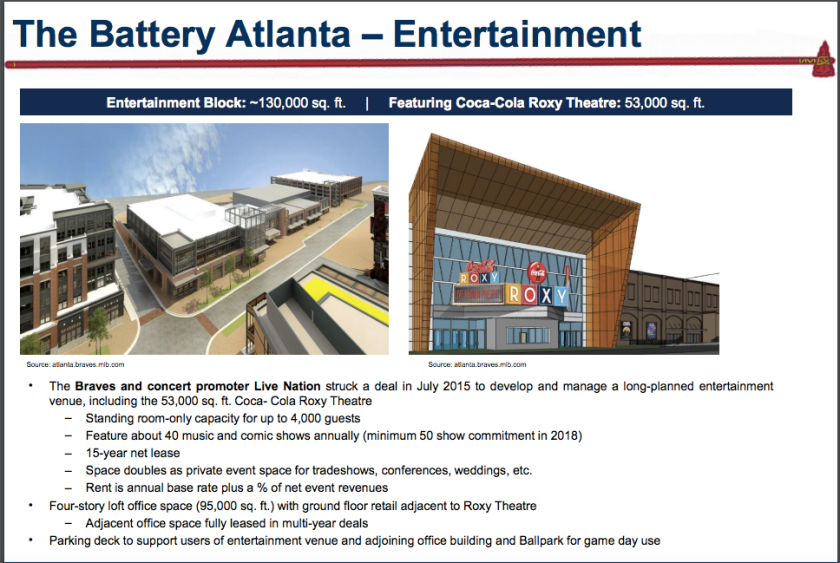

(Source: Liberty Media investor presentation)