I think there’s a reasonable argument to make that PICO Holdings (PICO) is conservatively worth 100% more than its price in the market today. The company has simplified its operations to focus solely on its portfolio of water rights located in Nevada and Arizona. I’ll describe the value driver of the rights in each state soon, but overall the water rights are a scarce asset that have and will only increase in value due to drought conditions as well as above average population growth.

PICO is focused on monetizing the water assets and using the proceeds to return capital to shareholders. This process has already begun as the company has simplified. In 2017 PICO sold their last non-water related asset, a stake in homebuilder UCP, for $115mm using the proceeds to pay a special dividend to shareholders. After a successful ramp of activity in the sale of water credits in 2017 and 2018, PICO repurchased 10.6% of outstanding shares in 2018. In 1Q19 the company repurchased $4.2mm of shares.

The sales in 2017/18 and other disclosures give us a good idea of where the market is currently valuing these assets. As I stated above, my conservative estimate is that the total value of the company today is 100% higher than today’s value. I’ll break down my view of the value of these assets below.

Nevada

In Nevada, the value driver of water rights is the above average population and employment growth, which have combined to create a housing shortage.

Each house needs about 0.5 Acre-Feet of water and as developers bring new houses onto the market, they must secure water rights that can be pledged to the area’s water utility for service. PICO has two main groups of assets in Nevada: Fish Springs Ranch and Carson/Lyon.

Fish Springs Ranch (FSR):

PICO owns a 51% stake in FSR, located 40 miles north of Reno. The water rights total 12,907 Acre-Feet (AF). Of this, 7,907 AF is available to be sold. The other 5,000 AF has received the necessary approvals from the the Nevada State Engineer, but federal rights of way would need to be updated before they could be monetized.

So what is this worth?

- In 2018 PICO sold 77 AF to a developer for $2.7mm or $35,000/AF.

- In 1Q19 86 AF were sold to a developer for $35,000/AF.

As the majority owner and managing partner of FSR, PICO has funded all of the operational and development costs. These costs accumulate as Preferred Capital, which accrues interest at LIBOR + 450bps. As of 12/31/18 the Preferred Capital balance stood at $181.7mm and was growing at >7%. As sales are made, the Preferred Capital will be paid out first. Applying the $35,000/AF value to the 7,907 AF available for sale, while paying out 100% of Preferred Capital first, you get the following value of the FSR assets:

I think this is a conservative estimate since it doesn’t include the additional 5,000 AF the company owns. I’m confident these additional 5,000 AF hold value, but given the uncertainty around development timing I’ll omit them for now.

Carson/Lyon:

A little more straightforward here, the company owns 3,500 AF along the Dayton corridor, east of Carson City and Lake Tahoe. In 2018 PICO sold 511 AF for $10.3mm or $25,000/AF.

3,500 AF @ $25,000/AF = $87.5mm in value.

Kane Springs:

PICO has an option agreement with a developer to sell the remaining 500 AF of water rights in this area at $6,358/AF, escalated at 7.5%/year from September 2017. The agreement expires in September 2019 with a cost to exercise of approximately $3.5 million. To date, the developer has made all required annual option payments ($60k/year).

Kane Springs Value = $3.5mm

Arizona

The value driver of the Arizona assets is a little different than Nevada. What PICO owns in Arizona is Long Term Storage Credits (LTSC). They are similar to the Nevada water rights as they are Acre-Feet of water that can be purchased by municipal or industrial users to satisfy water requirements. The driver here is the strain on the entire water supply due to the ongoing drought in the area and the effect it has on the Colorado River Basin and Lake Mead, where Arizona derives about 40% of its water.

If Lake Mead is expected to drop below 1,075ft, a Tier 1 shortage is declared. At Tier 1 (<1,075ft) Arizona would see their annual allocation from Lake Mead drop 320,000 AF. A Tier 3 shortage would push this to 480,000 AF annually. The states that share the reservoir (Arizona, California, Nevada, and Mexico) are doing everything they can to ensure shortages like this are avoided. On and off over the last 8 years they have been working towards something called the Lower Basin Drought Contingency Plan (DCP). The DCP would require additional water be held behind Hoover Dam in Lake Mead requiring a reduction in the volume of water that Arizona, Nevada, and California could use each year. So far, nothing has been agreed to. In a worst case scenario the Secretary of the Interior could use his/her power to determine what the shortage would be for each state.

In conjunction with the DCP group meetings, the Bureau of Reclamation presented its view on the likelihood of shortages. Without a DCP agreement, they see a 50% chance of a Tier 1 shortage in 2020 and between a 60-65% chance of a Tier 1 shortage in 2021-2026.

PICO’s assets in Arizona are perfectly positioned to benefit from either outcome here. Either the states take voluntary cuts under the DCP or they risk being subject to cuts when shortages are declared based on Lake Mead’s elevation (you can see the elevation levels of Lake Mead here http://mead.uslakes.info/level.asp). In either situation Arizona will need to replace hundreds of thousands of Acre Feet of water.

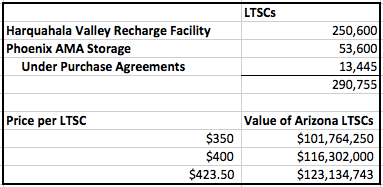

How much are the Arizona assets worth? There were three sales of LTSCs in 2017.

- In February 2017 PICO sold 100,000 LTSCs total to two parties (AZ Water Bank Authority and Central AZ Groundwater Replenishment District) for $25mm ($250/LTSC).

- In December 2017 PICO reached an agreement to sell up to 15,000 LTSCs to the Roosevelt Water Conservation District(RWCD) for a base price of $350/LTSC. The LTSCs may be purchased by RWCD at any time over the term of the agreement, which expires on December 31, 2019. Any purchases prior to December 31, 2017 will be at the base price of $350 per LTSC and any purchases of LTSCs under this agreement beginning January 1, 2018 will be at a price that is increased from the base price at 10% per annum.

- The company also currently has 1,150 LTSC under contract with Apache Sun Golf: 1,150 LTSC at prices ranging from $306.26-$375.18/LTSC, terminates 9/30/21

Given the escalator in the agreement from 12/31/17, the current market value would be $423.50/LTSC if RWCD exercises this agreement. I used a few possible prices and you can see the corresponding value break down below.

Conclusion

As stated in the opener, I think there’s a reasonable argument that PICO is at least 50% undervalued by the market.

Fish Springs Ranch $229.2mm

Carson/Lyon $87.5mm

Kane Springs $3.5mm

Arizona Base Case $116.3mm

Cash $12.6mm

Total Value $449.1mm

I intentionally was conservative in the estimation of value: not ascribing any value to some assets that are further from monetization and smaller in nature (including the Dodge Flat asset sale that closed in 1Q19 for $8.9mm of total proceeds). There is an argument to make that the supply/demand imbalance will push prices above levels that have been recorded in previous transactions. From what I’ve read, PICO’s water rights and constructed pipeline are the only source of water for developers in the Northern Nevada area.

While timing is uncertain I think the data points towards a short term need for water credits in both Nevada and Arizona. Monetization won’t be in a predictable straight line over the next 3-5 years. As part of the simplification of the business, PICO cut overhead costs in half, now expecting them to be $5.5mm going forward. This will free up more cash to be returned to shareholders as water rights sales are realized as well as help ease the lumpiness of any sales.

Overall, I think PICO offers investors a unique collection of assets that have a definite scarcity value and a nice margin of safety built in at current market prices.

I currently own shares of Pico Holdings (PICO). This article is not a recommendation to buy or sell.